The European energy storage market is evolving rapidly, with new markets and regulations emerging.

6 min read

As Europe’s electricity markets grow more complex, one thing is clear: battery energy storage systems (BESS) are no longer a side note, they’re becoming essential infrastructure. Whether enabling grid flexibility, capturing price volatility, or participating in ancillary services, BESS are now at the center of the energy transition.

But tapping into this potential is anything but straightforward.

From saturated ancillary markets in Western Europe to high-growth, subsidy-fueled momentum in countries like Poland and Spain, understanding where — and how — storage makes money is now a strategic imperative for investors, developers, and policymakers alike.

Europe’s BESS landscape is not uniform. The UK remains the market leader by capacity, but other countries are quickly catching up, each with unique market dynamics.

Germany, France, Spain, Poland, and Sweden represent key examples of where the European market is heading. Together, they offer a mix of mature, emerging, and transitioning storage environments. And each tells a different story about how BESS assets generate revenue.

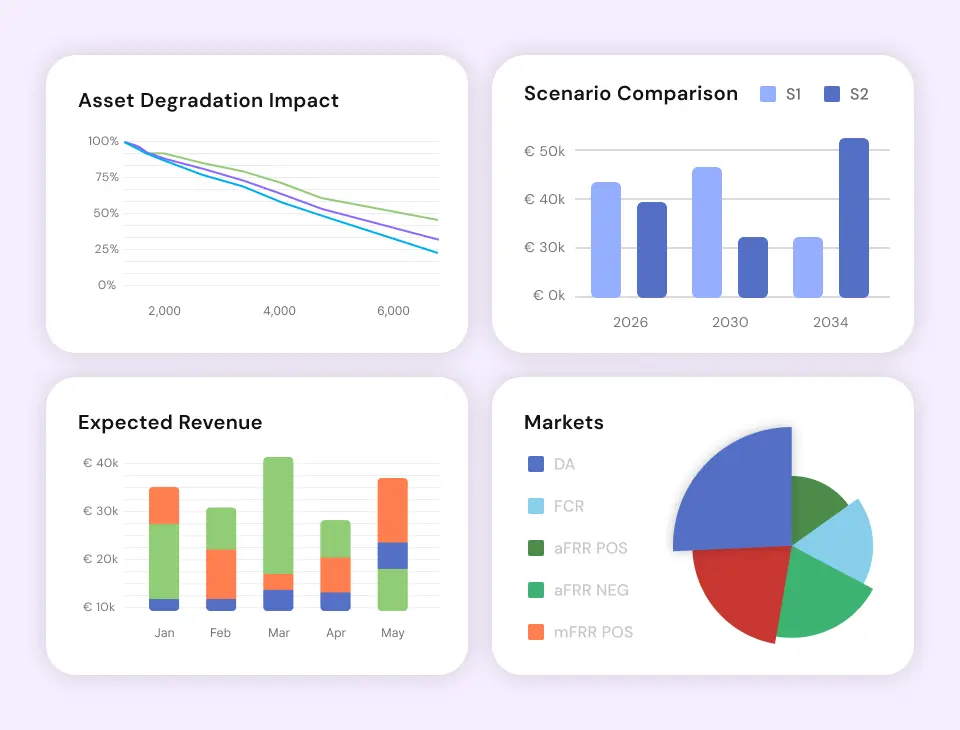

At its core, the value of BESS comes from one principle: flexibility. Storage systems can shift power across time and provide fast, responsive services to support the grid. But this flexibility must be monetized through specific market mechanisms. The three dominant revenue streams are:

Wholesale Markets: Capitalize on price spreads between low-cost and high-cost hours (energy arbitrage)

Ancillary Services: Deliver grid stability functions like frequency containment and restoration

Capacity Mechanisms and Subsidies: Provide backup capacity or unlock public investment support

In some countries, these are well-established. In others, they’re just beginning to emerge — with early-movers poised to capture the most value.

With generous capacity market auctions and a recently opened ancillary services market, Poland is now one of Europe’s most promising BESS investment destinations. Over 2.5 GW of BESS projects have secured contracts, many with delivery dates extending to 2029.

Revenue opportunities remain high — especially in aFRR and mFRR services — thanks to limited competition. But as the market matures, prices are expected to normalize, underlining the importance of early entry.

In 2024, France launched its secondary reserve market (aFRR), giving 2-hour BESS a substantial new income stream. While the primary reserve market (FCR) is nearing saturation, the aFRR opening has temporarily boosted returns. Still, increasing competition is beginning to compress margins.

The lesson? New market openings offer windows of opportunity — but only temporarily.

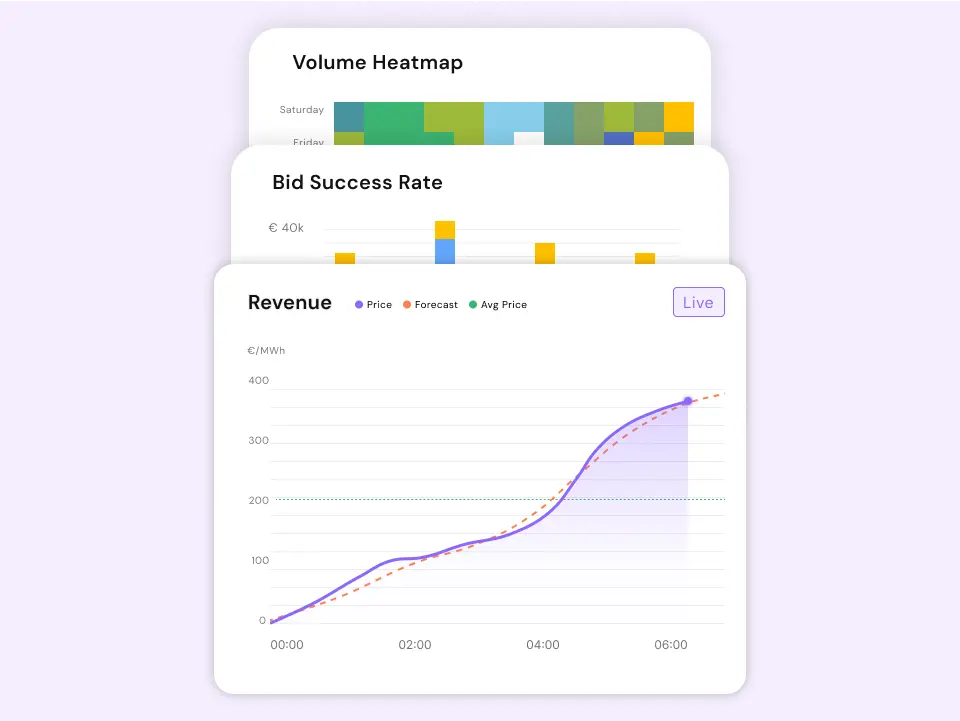

Germany’s BESS assets increasingly rely on Intraday trading and aFRR energy services. These markets offer high volatility and, with the right trading strategy, strong returns. However, traditional ancillary service markets are now crowded, pushing storage operators toward cross-market optimization strategies that require longer-duration assets and sophisticated route-to-market (R2M) capabilities.

In 2023, Spain awarded over 800 MW of BESS capacity through its PERTE program, providing substantial CAPEX grants for 4-hour systems. Spain is prioritizing long-duration assets to better support its renewable-heavy grid. While market revenues are still maturing, public support is reducing barriers to entry and unlocking bankability for new projects.

Historically, Sweden’s high FCR prices made it a lucrative market for 1-hour BESS. But as more projects enter the market — with 550 MW already prequalified for FCR-D — prices have started to decline. The lesson here is clear: price cannibalization can happen fast, and early entrants enjoy a temporary edge.

As Europe’s storage markets evolve, stacking multiple revenue streams is becoming essential. In the early days, operators could focus on a single service — like FCR. Today, success means balancing day-ahead trading, Intraday opportunities, and several layers of ancillary services.

This complexity requires expert trading strategy and deep market intelligence. That’s where Re-Twin Energy comes in. We model real-world market behavior — with no perfect foresight — to calculate realistic storage revenues across different durations and countries.

The launch of new services like aFRR in France or ancillary markets in Poland causes short-term revenue jumps. But these markets saturate quickly. **Timing is everything.**

Longer-Duration Storage is the Future

As simpler revenue streams like FCR decline, longer-duration systems (2-4 hours) become more attractive. They can trade across more markets, better handle volatility, and offer greater flexibility.

Cross-Market Optimization is Crucial

In saturated markets, single-source revenue strategies fail. Smart R2M providers optimize across wholesale, Intraday, and balancing markets — sometimes minute-by-minute.

Policy and Subsidy Design Drives Deployment

Public funding, like Spain’s PERTE program or Poland’s capacity auctions, plays a huge role in enabling BESS investments. But the long-term business case must stand on market fundamentals.

For energy storage investors, developers, and utilities, Europe offers rich — but complex — opportunities. The most successful projects will:

Enter early in emerging markets to benefit from higher prices

Build for flexibility, with longer-duration assets able to adapt to shifting price signals

Leverage smart trading and optimization, not just static revenue models

Align with policy trends, especially where subsidies de-risk capital investments

Storage is about timing, intelligence, and adaptability in a rapidly changing grid. Europe’s next phase of the energy transition depends on how well storage stakeholders rise to that challenge.

At Re-Twin Energy, we help storage asset owners and developers simulate, compare, and optimize BESS revenues across European markets. Our AI-powered digital twins and real-time analytics take the guesswork out of investment decisions.

About the Author

Florian Heise

Florian Heise is a energy-industry specialist with experience in consulting, logistics tech, and green-hydrogen development. As former head of strategic projects, he researched BESS and energy-storage markets across Germany and the EU. Today, he uses that knowledge as co-founder of Re-Twin Energy. Florian holds a Master’s in Finance & Accounting from Freie Universität Berlin and has even run a small coffee-import venture.

Ready to Transform Your Energy Strategy?

Unlock the full potential of your energy assets with Re-Twin Energy's cutting-edge Analytics & AI platform