Battery Energy Storage Systems (BESS) are growing rapidly in Germany. In 2024, for example, approximately 9,710 grid connection applications were submitted for medium- and high-voltage storage systems, totaling approximately 400 GW of power and 661 GWh of capacity. In contrast, only approximately 3,800 grid connection applications were approved, totaling approximately 25 GW and 46 GWh.[1]

As the grid becomes increasingly restrictive, storage systems can expect differentiated grid connections, such as static export limits, time-of-use limits, ramp-rate limits, and possibly redispatch requirements. At the same time, merchant markets require flexible and opportunistic dispatch strategies. Flexibility is rewarded in merchant markets, while controllability is necessary for grid functioning.

This white paper aims to quantify the economic impact of grid constraints on merchant BESS projects. Instead of assuming unconstrained market participation, we analyze the impact of differentiated grid constraints on dispatch strategies, revenue, and IRR results.

Key Findings:

Static export constraints have an impact of reducing revenues by 11-16% annually.

Time-based dispatch constraints during high volatility periods can cause revenues to drop by up to around 35-40%.

Combined constraint scenarios can reduce revenues by roughly 25-30% compared to unconstrained merchant scenarios.

Ramping constraints can cause revenues to drop by approximately 7-10% annually.

In all scenarios, the grid constraints have a significant impact on the overall IRR results. The results show the need for stress-testing the revenue assumptions for merchant storage under differentiated grid access conditions.

As grid scarcity increases, the profitability of storage is no longer driven by traditional market spread analysis. Storage value is increasingly being shaped by operational limitations and conditional access.

The German battery storage market has seen significant growth in the last few years.

In the transmission sector, the number of requests for large-scale BESS has increased substantially, driven by the rise in the level of investment activities and the associated competiton.

In 2024, the total number of grid connection requests for medium- and high-voltage BESS systems by German transmission and distribution system operators was around 9,710. This equals approximately 400 GW of power and 661 GWh of storage capacity. By contrast, only about 3,800 requests (≈25 GW / 46 GWh) have been approved in the same year.[1]

The government network planning scenarios show the growing structural mismatch between market-based deployment intentions and the rate of infrastructure development. With the Federal Network Agency’s Network Development Plan (NEP) scenarios predicting only 40-95 GW of large-scale storage capacity by 2045, the actual level of connection requests already exceeds 400 GW. This mismatch indicates that transmission infrastructure is poised to become the main bottleneck for large-scale BESS projects, especially at structurally congested points.[1]

With connection requests already exceeding the rate of grid development, grid transmission system operators will likely impose more stringent connection and operation conditions. This may include higher system support requirements as well as limits on maximum injection and/or offtake. In congested regions, projects may also face higher probabilities of curtailment and the application of allocation or priority rules for grid access. Additional operational requirements may apply, such as dispatch or scheduling obligations.

The economic implications for projects are straightforward: BESS projects can no longer use generic grid parameters. Site-specific grid restrictions, curtailment risk, allocation rules, and operational restriction scenarios, including downside scenarios, must be formally modeled in economic projections.

The increase in applications is a result of shifting market incentives as well as investor interest. Indeed, the price volatility, ancillary services, and flexibility premiums all provide a stronger case for the deployment of storage.

Nevertheless, this expansion is taking place in a grid that was not intended for extensive, bidirectional, dispersed flows. It is occurring in a transmission network that was not designed for large amounts of decentralized, bidirectional flexibility resources.

A structural change is taking place:

Grid access is becoming an increasingly defining variable for project feasibility.

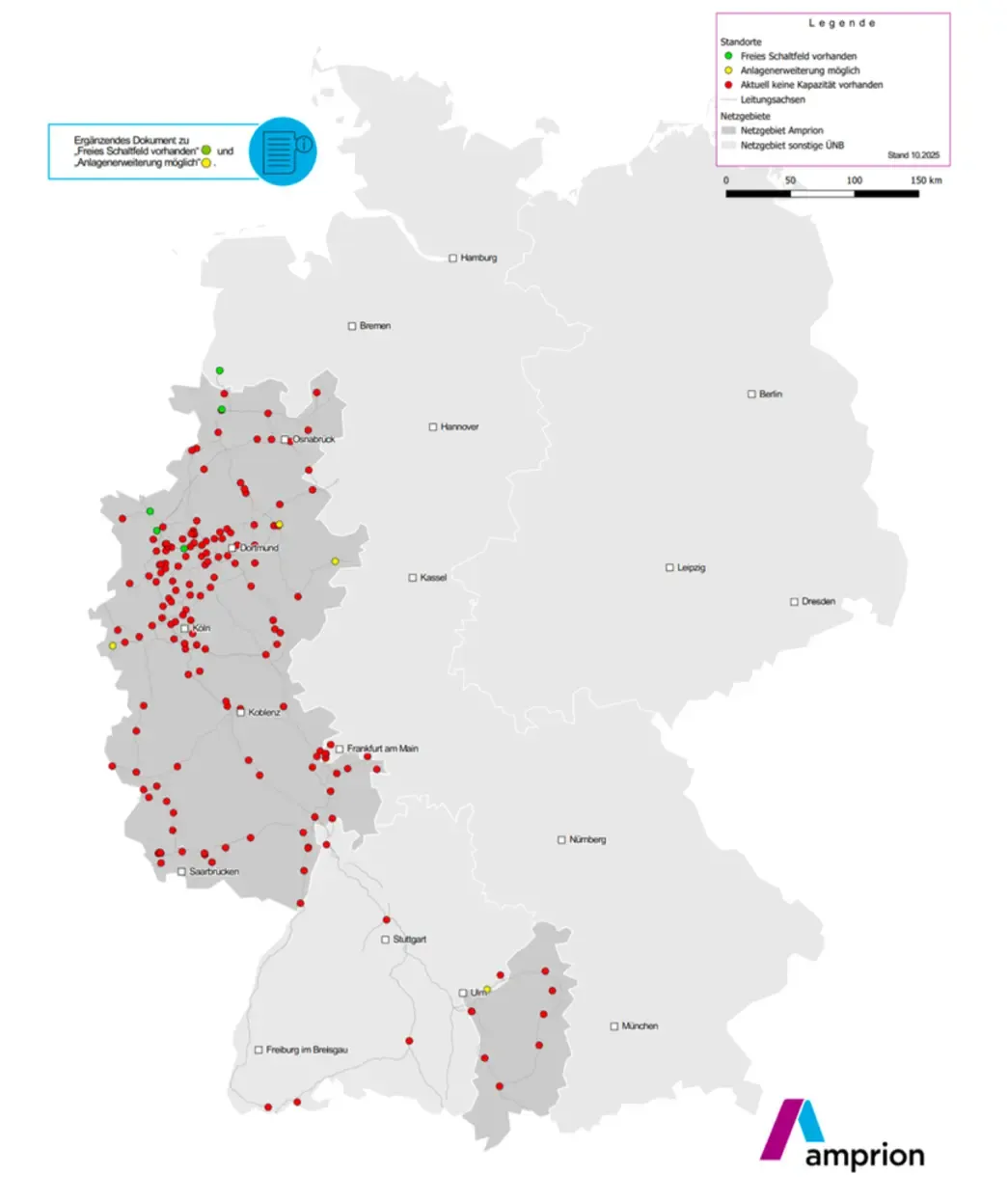

Figure 1. Transmission-level BESS connection points and switchgear bay availability in the Amprion TSO area (data as of Q4 2025)

Figure 1 shows the distribution of connection points and the availability of switchgear bays within the Amprion TSO area. Many substations show limited availability of free bays, particularly in regions with high application volumes. The map reflects switchgear availability and does not directly indicate the available network connection capacity (NAK).

In parallel to regional saturation, application volumes have increased sharply over time.

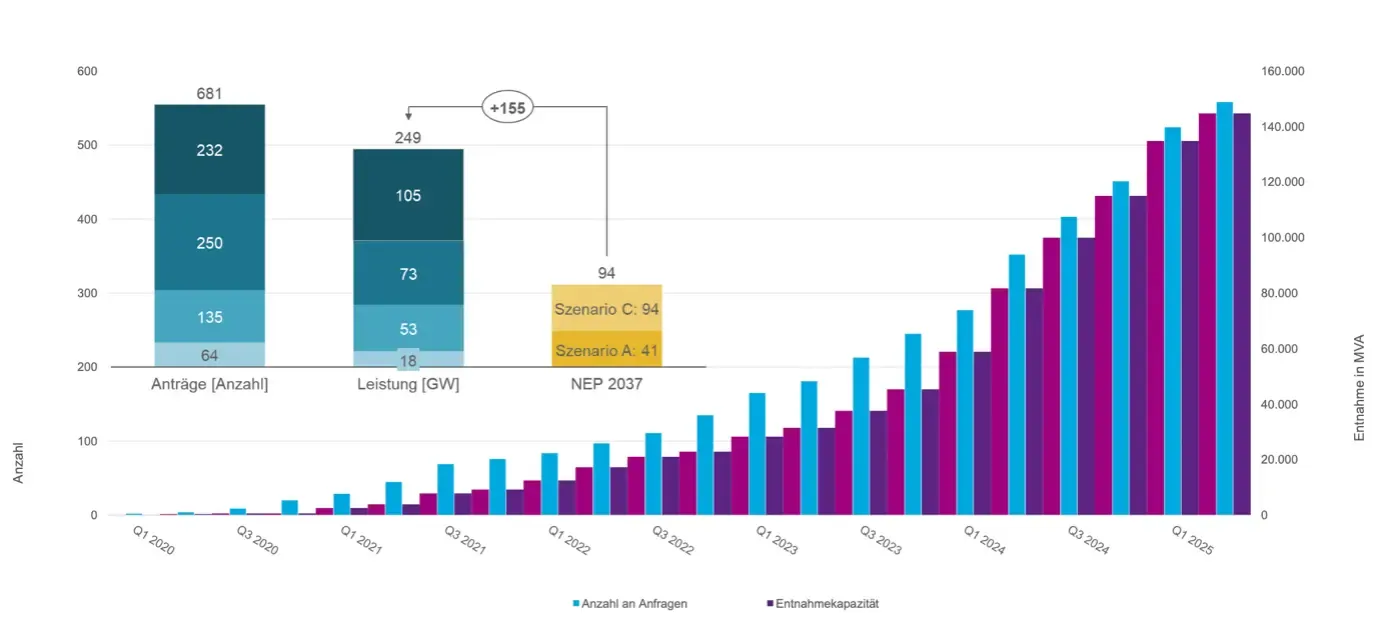

Figure 2. Growth in BESS Connection Requests and Capacity Compared to NEP 2037 (data as of Q4 2025)

Note: “Anträge Anzahl” refers to number of applications; “Leistung GW” refers to requested withdrawal capacity in GW; “NEP 2037” refers to planned storage capacity under the German Network Development Plan.

Figure 2 illustrates the strong growth in connection applications (“Anträge”) and cumulative requested capacity (“Leistung”) since 2020. Already in early 2025, the number of applications and the requested capacity are well above the levels assessed in the NEP 2037 planning scenarios.

The gap between requested capacity and grid expansion plans reveals a structural conflict: investment is guided by market signals and short-term profitability prospects, whereas grid expansion follows long-term infrastructure planning processes defined within the German Network Development Plan (NEP). The NEP is based on a scenario framework (“Szenariorahmen”) that considers different consumer and demand groups and is updated every two years.

This, however, does not mean that projects will be rejected outright. On the contrary, grid access is likely to be granted with an increasing number of differentiated operational constraints that will ensure system stability. These may include time-of-use availability, power limits, curtailment requirements, congestion-driven dispatch constraints, or redispatch obligations. The key analytical question, therefore, is not whether storage can gain grid access, but how each of these different types of grid restrictions affects the economics of BESS projects, and which configurations of these restrictions are commercially viable.

From a system perspective, transmission grid expansion has been identified as a structural bottleneck for renewable integration and flexibility deployment.[2]

Therefore, the rapid growth in BESS applications occurs in a context where:

Physical grid capacity is location-specific,

Connection processes are increasingly competitive,

Operational constraints are likely to evolve in parallel with congestion management requirements, including dispatch limitations, ramping rules, and redispatch participation.

This sets the stage for the analytical framework applied in the following sections. We translate differentiated grid-access restrictions into explicit modelling assumptions and systematically assess their impact on realized BESS profitability across scenarios.

Germany has a single bidding zone in its wholesale electricity market. This means that a common price signal is created at the national level, independent of local transmission constraints. Therefore, the German transmission system operators (TSOs) must actively control physical congestion through redispatch and congestion management systems, particularly on physically limited north-south transmission lines.

From an investment point of view, this creates a strong price signal. However, from the perspective of grid operators, this signal can be incomplete. Wholesale spreads and ancillary service prices identify monetization opportunities, but they do not capture congestion exposure at the local level.

In practice, zonal pricing does not eliminate local congestion exposure. At saturated nodes, redispatch measures and operational constraints can limit effective dispatch flexibility despite identical wholesale price signals. For project-level economics, this means that price spreads alone are insufficient; applicable grid constraints ultimately determine realizable revenues.

The congestion management volumes in the German market are a good example of the significance of this problem. According to the Bundesnetzagentur Monitoring Report 2023, total congestion management volumes amounted to 32,772 GWh (or 32.8 TWh) in 2022, with corresponding system costs of approximately €4.2 billion. [3] However, it should be noted that electricity prices were exceptionally high in 2022 due to the energy market disruptions following the war in Ukraine, which partly amplified the reported congestion management costs. Nevertheless, these figures illustrate that redispatch is not a marginal operational adjustment, but a structural feature of system operation.

For storage investors, this creates a dual reality:

Market dispatch is economically optimized.

Grid operation is physically constrained.

Wholesale pricing curves do not show the realization risk that results from this.

In high-renewable systems, dynamic operating limitations are becoming more important in addition to static export or connection limits. To maintain system stability, transmission system operators may implement operational requirements that are time-dependent or ramp-rate related.

From an investment perspective, such dynamic constraints reduce short-term optionality value and can limit the ability to fully capture intraday price spreads during high-volatility periods.

In merchant backtesting conducted by market participants such as traders, the common assumption is that market access is unconstrained. However, this is not necessarily the case for a project that is subject to grid intervention constraints, redispatch obligation constraints, or connection constraints. As a result, two projects that are exposed to the same price spread may exhibit different backtest outcomes depending on their location within the grid.

Studies show that the economic value of flexibility assets is not only driven by price volatility but also by the underlying transmission topology and congestion patterns. For investors, this implies that two projects facing the same price spread may generate significantly different revenues based on grid location and operational constraints.

From an investment perspective, location is more than a technical parameter; it determines the applicable connection framework, potential dispatch limitations, curtailment risk, and ultimately revenue realization.

In conclusion, this paper seeks to quantify the impact of various constraints imposed by the grid on the economics of a BESS project. Through a systematic comparison of the various types of constraints, such as time-of-availability, static power limits, non-firm transmission access, and curtailment risk, as well as dispatch, ramp, and redispatch constraints, the paper aims to show the differences in their effects on project economics.

Short-term dispatch flexibility is constrained by ramping limits, which define the maximum rate at which a storage asset can increase or decrease its injection or offtake.

A 10 MW/20 MWh BESS in a standalone configuration, limited to a maximum of 2 cycles/day, 90% efficient, and multi-market merchant BESS participation, is simulated using 2024 historical data as an unconstrained reference case, and compared to differentiated grid constraint scenarios, including static export limits, time-based dispatch restrictions, ramp-rate restrictions, and redispatch obligations, in terms of dispatch, revenues, and IRR.

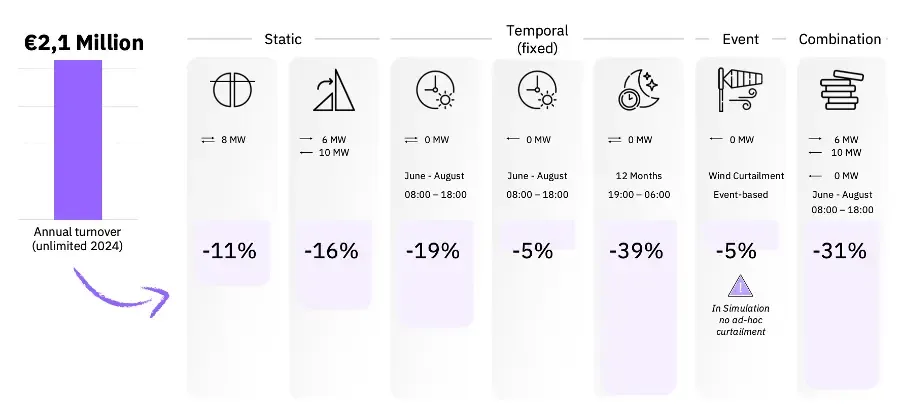

Under the unconstrained simulation, the revenues generated by the BESS are approximately €2.1 million annually, or €210,000/MW.

3.1 Static Capacity Limitations

In the first scenario, symmetric static power limitations are applied. The maximum charging and discharging capacity is reduced from 10 MW to 8 MW, while the energy capacity remains unchanged at 20 MWh. This effectively lowers the asset’s C-rate and limits its ability to fully monetize short-duration price spikes. Under this symmetric restriction, annual revenues decrease by approximately 11%.

In the asymmetric case, charging capacity is reduced from 10 MW to 6 MW while discharge capacity remains at 10 MW. This disproportionately constrains the asset’s ability to exploit negative-price and ancillary-service windows, resulting in a stronger revenue reduction of approximately 16%.

Overall, static power caps reduce capturable revenues primarily by limiting participation in high-value dispatch periods rather than by proportionally reducing total energy throughput.

3.2 Time-Based Operational Windows

The second scenario includes time constraints on dispatching within specific hours.

A prolonged night-time restriction applied over the full calendar year (January-December, 19:00-06:00) leads to a revenue reduction of about 39%, which represents the effect of restricting dispatches within structurally volatile times. This significant impact reflects that evening and night hours frequently concentrate intraday price spreads, balancing activations, and short-term volatility events in high-renewable systems. Restricting dispatch during these hours removes access to structurally high-value trading windows, limiting both charging in low-price periods and discharging into high-price evening peaks.

In one of the cases, dispatches are restricted during peak solar times (June-August, daytime period between 08:00 and 18:00). In another case, only discharging is restricted during this time.

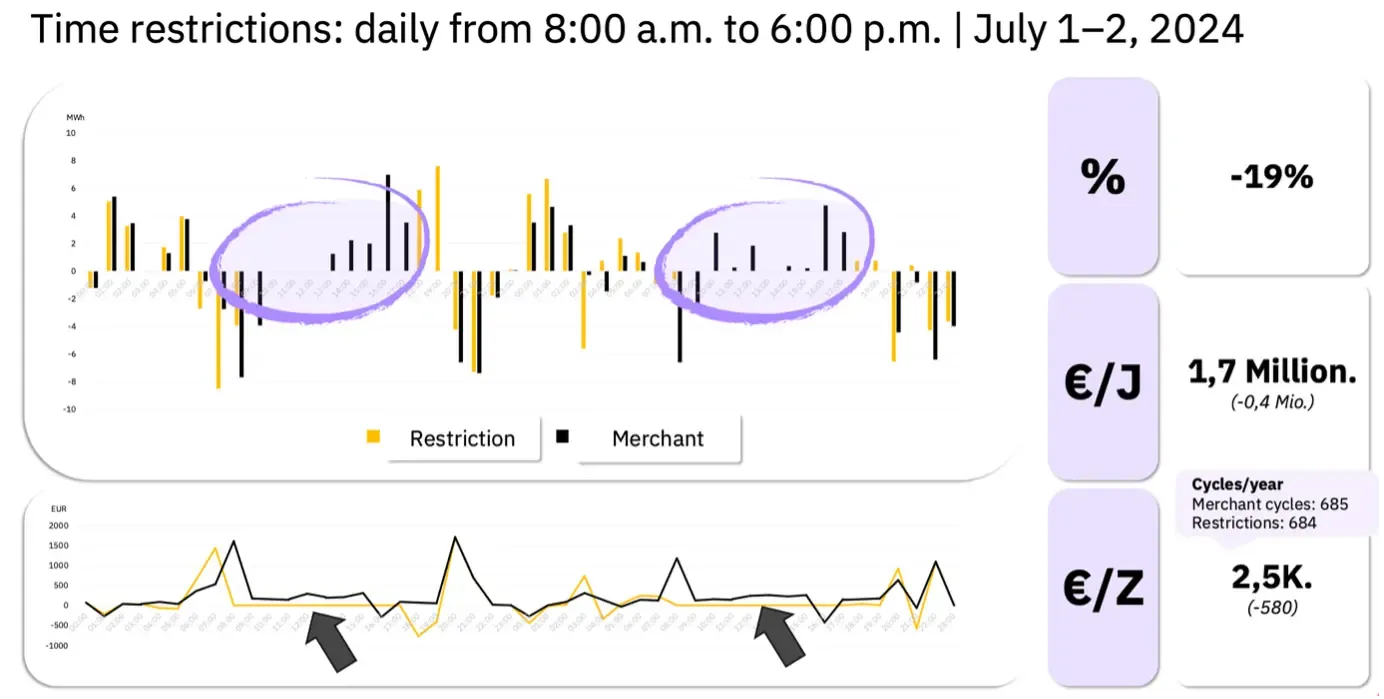

The following graph shows the effect of a daytime operating schedule on intraday dispatches and revenue.

Figure 3. Intraday Dispatch Under Time-Based Restriction (08:00–18:00)

Figure 3 compares the merchant dispatch strategy (black) with dispatch under the daytime restriction (yellow). The restriction prevents charging and discharging between 08:00 and 18:00, limiting the ability of the system to exploit intraday price spreads during peak solar hours.

The lower panel illustrates the resulting impact on daily revenues, showing how the restriction reduces volatility capture despite a similar number of annual cycles.

Although dispatch flexibility within the day is reduced, the overall number of cycles per year remains largely unchanged.

Revenue impacts:

Revenue decreases by approximately 19% under full time-based restriction.

Revenue decreases by approximately 5% under the discharge-only restriction.

The following figure consolidates the revenue impact across the different constraint scenarios discussed above.

Figure 2. Growth in BESS Connection Requests and Capacity Compared to NEP 2037 (data as of Q4 2025)

Figure 4 illustrates the relative revenue reduction for static, time-based, and combined constraint scenarios. The outcome indicates that the imposition of constraints on certain high-value hours can have a disproportionately large effect on annual revenue.

Notably, the number of cycles in a year is relatively consistent across a number of scenarios. This has a number of implications, including that the revenue per cycle will be reduced.

3.3 Combined Constraint Effects

When static and time-based constraints are combined:

Revenue decreases by approximately 31%

This shows that operational constraints can have compounding effects rather than additive effects. Projects at constrained nodes may thus have structurally lower revenue realization than unconstrained merchant backtests.

3.4 Ramping Constraints and Flexibility Reduction

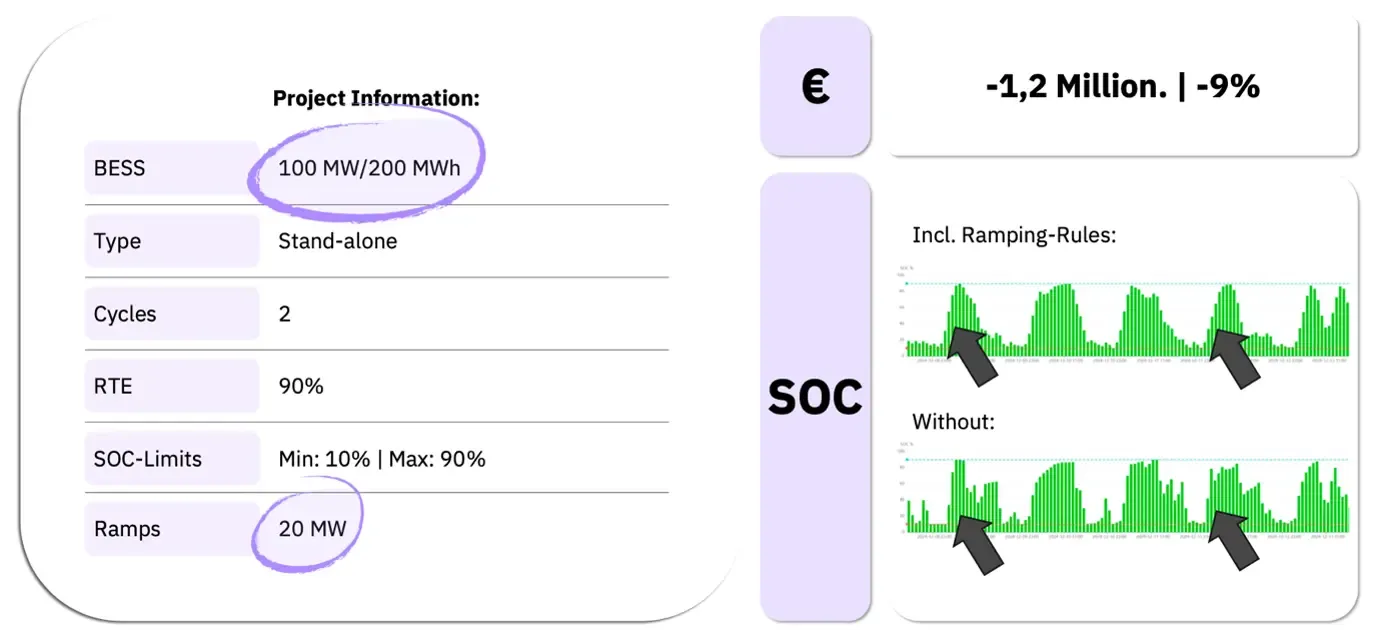

The final scenario evaluates ramping limits, which restrict the speed at which a battery may adjust output within defined intervals.

Although the reference case is based on a 10 MW/20 MWh asset, the ramping analysis is performed on a 100 MW/200 MWh basis to represent transmission-scale projects that are subject to absolute ramp rate constraints (e.g., MW/15-minute interval). Because ramp rate constraints are expressed on an absolute scale rather than a relative scale as a percentage of the total power output, their economic implications are only significant at utility-scale system sizes.

Simulation results for a 100 MW / 200 MWh system with 15-minute ramping steps show:

Revenue decreases by approximately 9%

Figure 5. Impact of Ramping Constraints on Dispatch and Revenue

Figure 5 compares dispatch behavior with and without ramping constraints. The ramp limit of 20 MW per 15-minute interval smooths SOC trajectories and reduces short-term volatility capture. In the simulated case, this results in a revenue reduction of approximately 9%, corresponding to around €1.2 million annually.

For all cases, the revenue losses vary between 5% and 31%, depending on the type and time of constraint.

The results indicate that ramping constraints are not a marginal technical consideration but a potential determinant of realized IRR under volatile market conditions.

The analysis leads to several practical conclusions for developers, investors, and asset managers.

a) Grid constraints materially alter revenue outcomes.

Depending on the type and timing of the constraint, annual revenues can be reduced between 5 and 39 percent. Profitability is thus not driven by market spreads alone but is subject to specific operational conditions of the respective connection.

b) Constraint type matters more than constraint presence.

Static export limits, time-based restrictions, and ramp-rate have materially different economic impacts. Time-dependent constraints during high-volatility periods produce the largest revenue reductions.

c) Merchant backtests require constraint-adjusted sensitivity analysis.

Unconstrained merchant assumptions can materially overstate expected revenues. Bankability assessments should explicitly incorporate differentiated grid-constraint scenarios.

The growth in BESS in the German market is heavily driven by the strength of wholesale price signals and volatility capture opportunities. However, the results show that, the key driver for profitability is not based solely on the wholesale price spread, but rather the grid constraint model applied at the specific connection node.

The analysis has shown that, across the simulated scenarios, the reduction in revenues varies between 5 and 39 percent, dependent upon the specific constraint applied and the timing thereof. The static export constraint reduces revenues by 11-16 percent, while the time-dependent constraint applied during periods of high volatility has shown the greatest impact. The ramping constraint, although not having a material impact upon total energy throughput, has shown a 9 percent reduction in revenues, highlighting the value of short-term flexibility.

As demonstrated, when combining multiple constraint scenarios, the reduction in revenues is as high as 31 percent, which has a significant bearing upon the IRR assumptions applied. As the grid becomes more constrained, it is critical that backtests applied for merchant projects, assuming unconstrained dispatch, should specifically include cases with varying grid constraints.

[4] International Energy Agency (2023). Electricity Grids and Secure Energy Transitions. Paris: IEA. IEA

[5] Bundesnetzagentur and Bundeskartellamt (2023). Monitoringbericht Energie 2023. Bonn. Bundesnetzagentur

[6] ACER (2024). ACER Market Monitoring Report 2024 – Electricity Wholesale Markets Volume. European Union Agency for the Cooperation of Energy Regulators. ACER

[7] TransnetBW (2026). Übertragungsnetzbetreiber führen 'Reifegradverfahren' für Netzanschlussanträge von Speichern und Großverbrauchern ein. TransnetBW

[8] Joskow, P. L. (2019). Challenges for wholesale electricity markets with intermittent renewable generation. The Energy Journal, vol. 40, no. 2. DOI: 10.1093/oxrep/grz001. The Energy Journal

[9] Czock, B. H., Sitzmann, A., and Zinke, J. (2023). The place beyond the lines – Efficient storage allocation in a spatially unbalanced power system. EWI Working Paper 23/01. EWI

About the Author

Begüm Divrik

Begüm Divrik works in Business Development at Re-Twin Energy, focusing on market research and growth across European energy markets. Her work includes identifying new opportunities for the Re-Twin platform, supporting market analysis, and building relationships within the renewable energy and storage ecosystem. Previously, she worked on energy market research and digital energy platforms in the German energy sector. She is currently studying Renewable Energy, Waste and Water Management in Berlin.

Ready to Transform Your Energy Strategy?

Unlock the full potential of your energy assets with Re-Twin Energy's cutting-edge Analytics & AI platform